On July 22, the II International Congress «Digital Money and ICT Governance in the EU: New Legal and Technological Standards» will take place in collaboration with BAES y BlockchainFUE , of which Zitycard is a founding partner and developer of Didinet.

Didinet is a research project for testing and using electronic money based on blockchain technology.

The goal of the University of Alicante is to establish a foundation for creating future regulation of European cryptoassets, including stablecoins, NFTs, service tokens, and others.

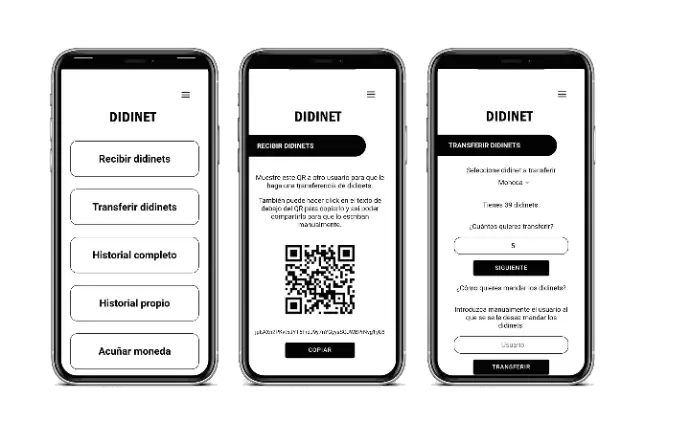

The app will allow Didinet researchers to have a testing environment in which they can work with tokens and assets, helping to establish the basis for future regulation of cryptoassets. Within the app, users can mint new, versatile tokens adaptable to any legislation or emission conditions, perform transfers between users, and view a history of transactions made.

At a time when cryptocurrencies, with Bitcoin as the main reference, are making headlines, many do not know that they are based on blockchain technology—the underlying technology used to create digital money. Specifically, stablecoins are cryptocurrencies that are referenced to a stable currency, differentiating them from Bitcoin's volatility.

Bitcoin can be "mined" (or obtained) by anonymous users, while stablecoins are generated by an entity responsible for holding and distributing them. This model is known as the central bank model.

Another major difference is that stablecoins are backed by a basket of stable value assets, such as currencies or commodities.

Objetivos of Didinet

The objectives of the Didinet research project are as follows:

- Determine the concept, legal nature, and regulation of digital money.

- Assess the scope and potential for decentralized ledger annotations and their legal effects over time.

- Analyze Blockchain-supported payment networks and/or services associated with cryptocurrencies.

- Mitigate security risks, systemic risks, and user protection risks within payment networks, focusing on:

– New vulnerabilities.

– Liquidity risks.

– Deposits and prudential regulations.

– Limiting cybersecurity risks.